ACADEMIC INTRODUCTION

& SOURCES

A practitioner's case, made auditable.

Not a peer-reviewed study, and it does not pretend to be one: a structured, sourced, deliberately falsifiable practitioner's analysis of a single firm at a single moment, built to behave in an academically usable way — auditable, attributable, datable.

If Ross King's robot scientist asks whether science can become self-executing, his program-money asks whether money can become self-executing. This book asks the missing fintech question: what compliance, identity, and institutional wrapper would make self-executing money safe enough to touch the real economy?

A practitioner's analysis, tagged claim by claim

This book is not a peer-reviewed study, and it does not pretend to be one. It is a structured, sourced, and deliberately falsifiable practitioner's analysis of a single firm — Revolut — at a single moment, in mid-2026, written by someone who has built and licensed regulated financial infrastructure rather than studied it from the outside. Every load-bearing claim is tagged in the text as one of three things: a fact drawn from public reporting, an inference I am willing to defend, or a labelled speculation about what could be built.

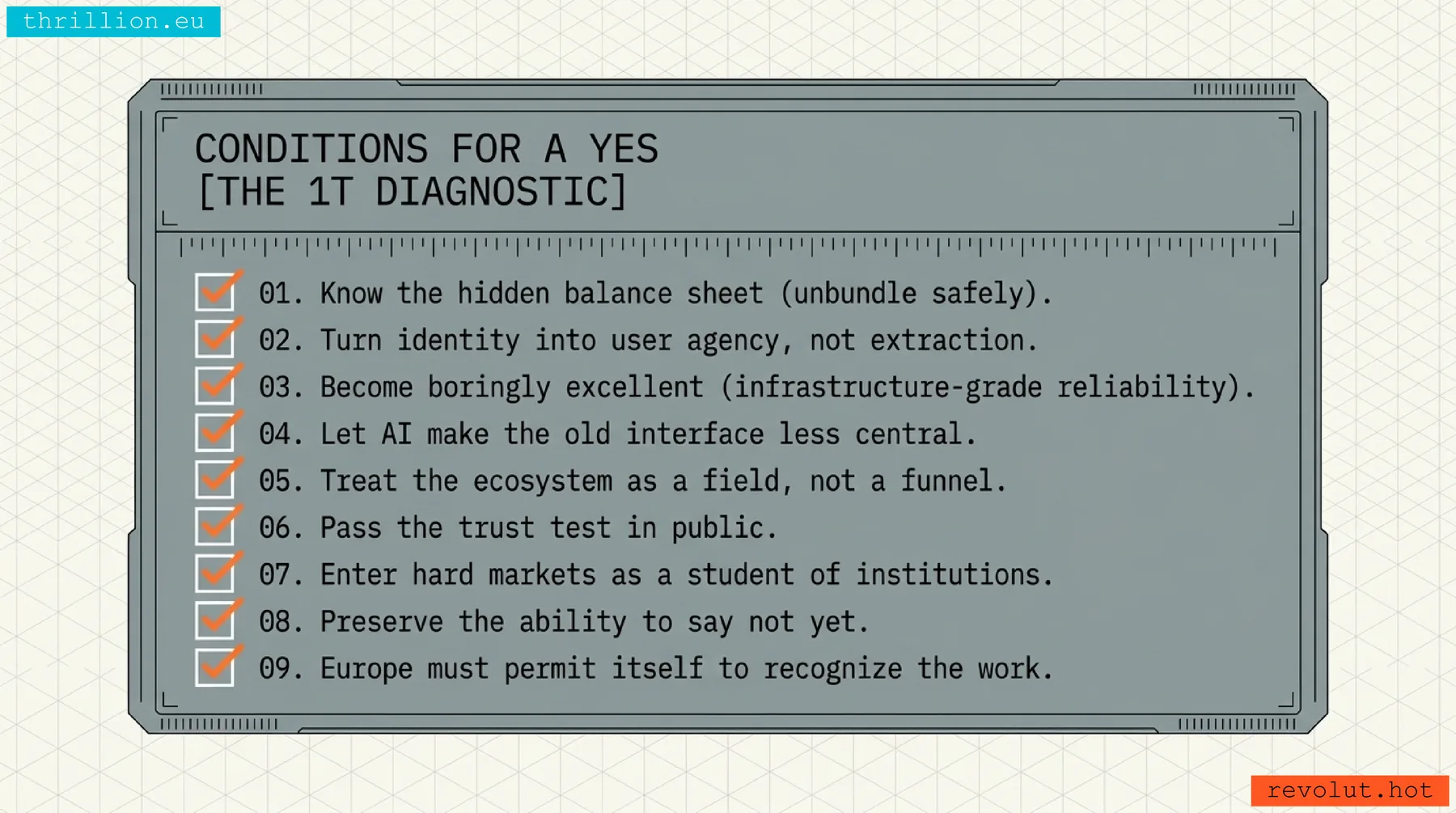

A short decision method — the "Compass" — runs throughout, decomposing each strategic "no" into what is genuinely hard, what is merely soft, and what only needs checking. The point of all this apparatus is to make a non-academic book behave in an academically usable way: auditable, attributable, and datable.

Disciplined foresight, not retrospective proof

An economist I speak with often, who studies exchange rates for a living, once put the difference between us this way: the scientist certifies what has already happened and can be measured; the entrepreneur reasons about what could be made to happen, which no instrument can measure in advance. This book lives in that second register — and whatever academic value it has lies precisely there.

It is a documented, time-stamped record of how a practitioner reasons forward under uncertainty, with the premises left exposed, so that a reader can do what scholars do: test the facts, contest the inferences, and, in a year or five, score the speculations against what the world actually did. A forecast with its reasoning shown is more useful than a forecast merely asserted — and far more useful than the silence practitioners usually keep.

The literatures it touches

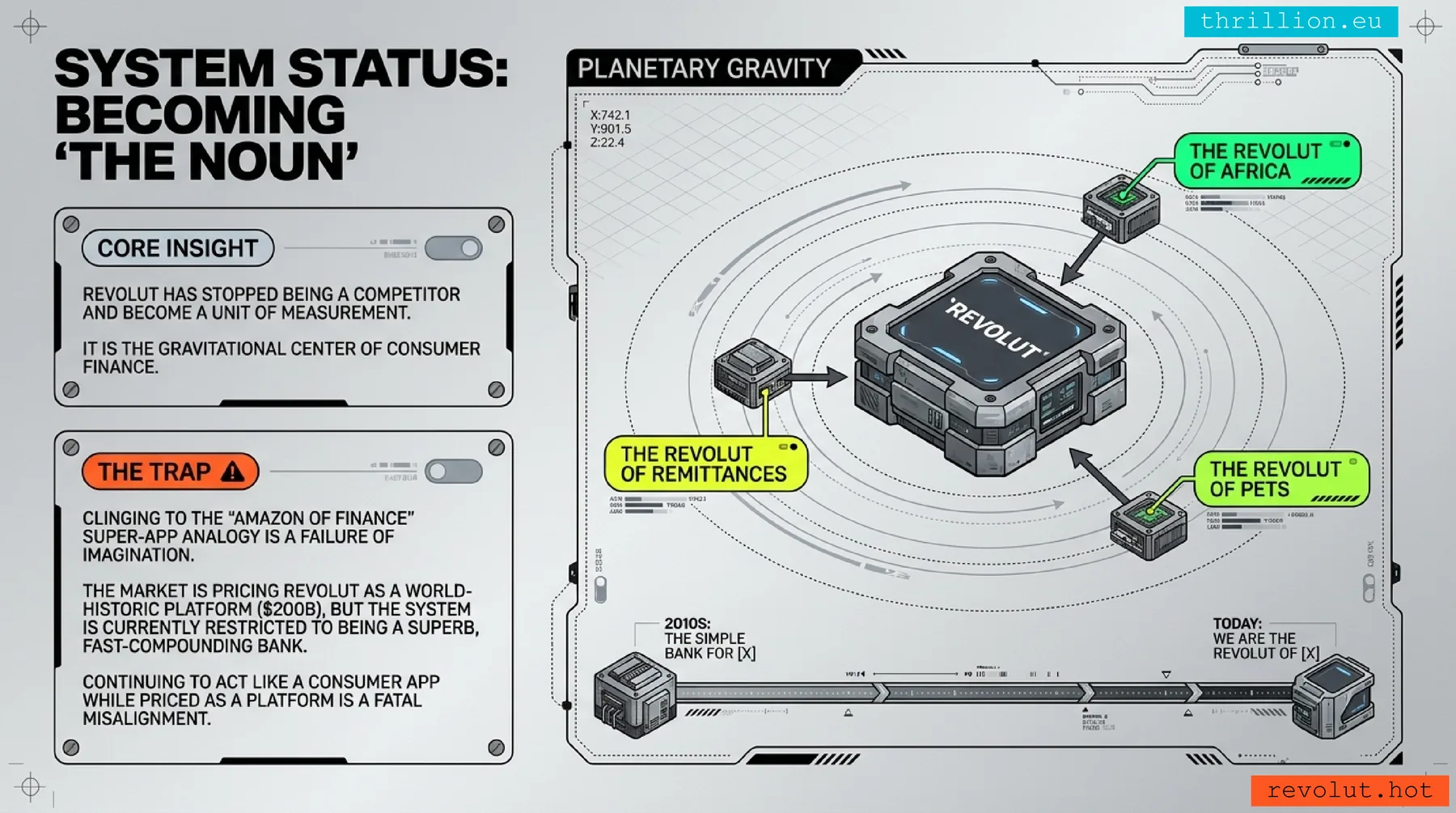

The central question is not whether Revolut is already a trillion-dollar company, but which assets it has already paid for — verified identities at scale, a compliance stack, transaction intelligence, banking permissions, stablecoin rails — could become new lines of profit under the right operating model. This is the spirit of Girotra and Netessine's risk-driven business model: the largest moves are often not new products but changes in which decisions get made, when, by whom, and why.

The monetary chapters — stablecoins as cross-border settlement rails, currency baskets and a synthetic unit "no one elected," seigniorage when private rails displace correspondent banking — are an operator's hypotheses about the same questions Itskhoki and his co-authors study with formal models: why a handful of currencies, above all the dollar, dominate global settlement; what monetary sovereignty costs; why exchange rates disconnect from fundamentals. I look at the other end of the same problem.

The most direct theoretical bridge. King's 2016 proposal to use computer programs themselves as money — "program-money," whose defining new property is agency — is the conceptual starting point for my question: what would programmable money need in a regulated world? My answer is that agency alone is not enough: it needs embedded compliance, identity, provenance, auditability, error-governance, and privacy-preserving disclosure. His separate argument — that machine reasoning should be expressed in a formal, logical language so its output can be tested and trusted rather than left a black box — is, in a different domain, exactly what regulated finance now needs.

The "Compass" is offered, more modestly, as a small reusable heuristic for decomposing a strategic choice when the relevant facts are not yet knowable — in the spirit of work on targets and structured trade-offs, though the book uses the idea informally rather than formally.

A large part of the book treats regulated digital identity as financial infrastructure: reusable, bank-grade, consented verification as a path to portable trust — and contrasts that route with the more speculative proof-of-personhood experiments now competing for the same role.

That last bridge deserves a sentence of its own, because it is where the book is most speculative and most often misread. The step after programmable money may be agentic money — not money with a personality, and not money free to improvise like a rogue trader, but money with bounded agency: a unit of value that could know its issuer, holder, purpose, jurisdiction, maturity, risk score, provenance, and permitted uses; refuse a transaction, request a missing proof, expire, or settle automatically once its conditions are met. That is the regulated version of King's program-money thesis — money as active code, constrained by law, identity, policy, and audit. As of 2026 the milder form is no longer theoretical; it is being built.

A map of researchable questions

The book does not claim to prove a theory. It proposes a map of researchable questions — and those questions, not any single prediction about Revolut, are the part of the manuscript most likely to be of use to a researcher.

- Can a bank-grade digital identity become reusable infrastructure?

- Can programmable obligations become legally legible without becoming surveillance?

- Can models trained on financial event-sequences become an external trust engine?

- Can stablecoins become boring settlement rails rather than speculative assets?

- Can a European fintech become a case study in regulated trust at software speed?

Influences

This work was shaped by, and is in dialogue with, the published research of several scholars, named here as influences and interlocutors — not as endorsers, and with no implication that any of them has read, reviewed, or approved it. The forward-/backward-looking frame I owe directly to conversations with Oleg Itskhoki (Harvard) and to his work on exchange rates and dominant currencies. The business-model spine reflects Serguei Netessine's (Wharton) risk-driven framework. The argument for logic-based, verifiable AI — and the example of a boundary-crosser who spent years combining fields the academy treated as incompatible — draws on Ross D. King's (Cambridge / Chalmers) work on robot scientists, on formalising knowledge so machines can be trusted, and on his proposal of computer-programs-as-money. Work on decisions under uncertainty by Ilia Tsetlin (INSEAD) informs the method more lightly. Whatever is wrong in these pages is mine, not theirs.

Sources & method

Everything factual is drawn from public reporting and primary documents through June 2026, and the load-bearing figures were checked rather than assumed. Everything speculative is labelled as speculation — on purpose. Keeping the two apart is the only thing that earns a visionary book the right to be visionary.

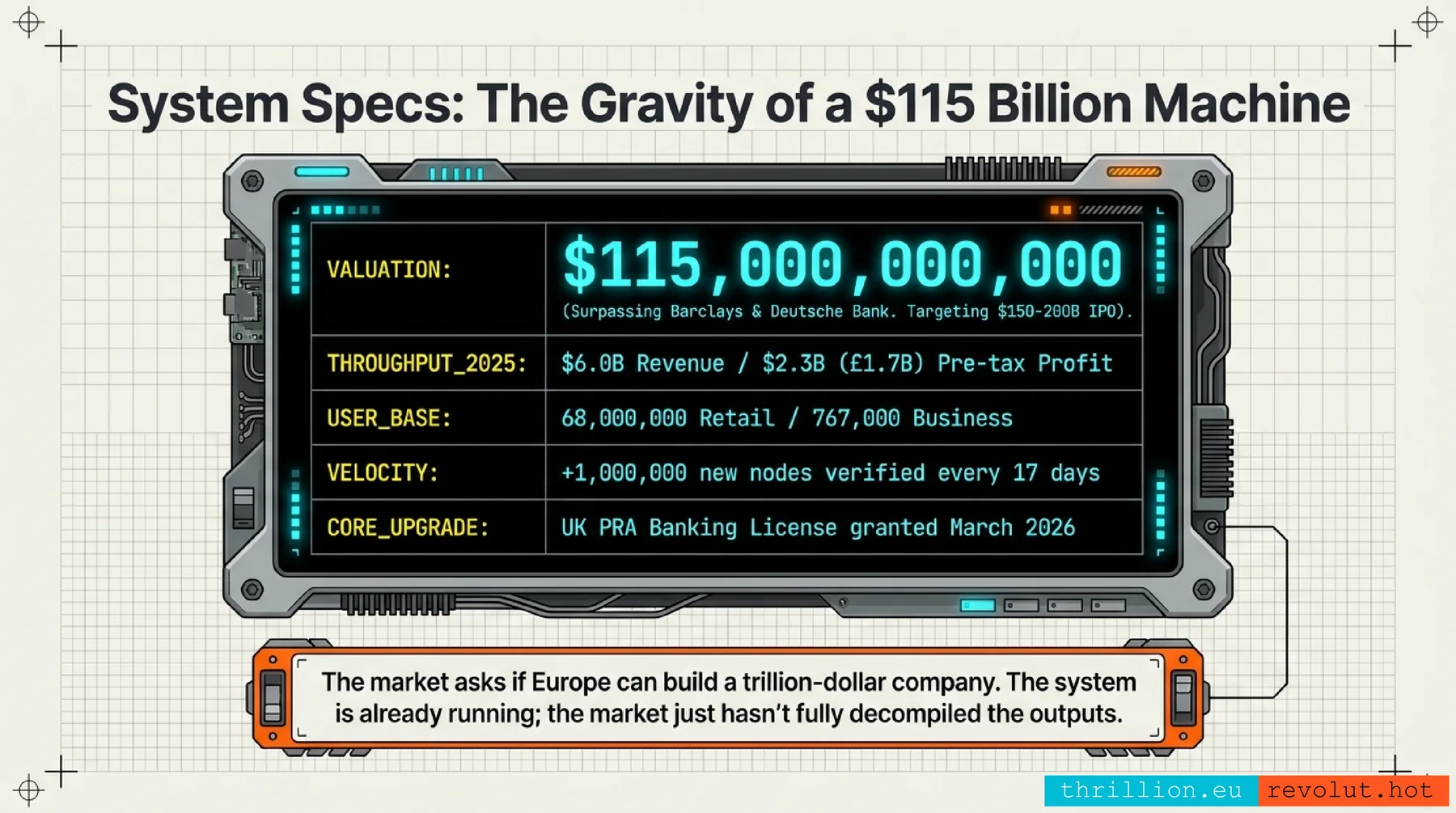

Everything factual — valuations, customer and business numbers, the leadership change, the licences, PRAGMA's architecture and gains — is drawn from public reporting and primary documents through June 2026, and the load-bearing figures were checked rather than assumed. Everything speculative is labelled as speculation, and there is a great deal of it, on purpose, because that is what this book is for.

The provocation chapters draw on my own research dossiers, distilled through NotebookLM and local AI models and then written up here; where those dossiers describe my hypotheses rather than established facts, or where Revolut's actual strategy diverges from the idea I'm flying, I've tried to say so in the text — including two places where my own research caught me overclaiming and I corrected myself in public. Characterisations of Nik Storonsky reflect public record, third-party behavioural analysis, and my own general impressions; no private correspondence is quoted, and personal matters are deliberately excluded.

Where each claim sits

Confirmed

Public reporting & primary documents: the FY2025 results; the full UK bank launch; the US national-bank-charter filing; the $75bn secondary; PRAGMA's existence and published metrics; the AIR launch; the private-banking unit and FCA approval.

Reported, not yet completed

The mooted ~$115bn secondary; the $150–200bn IPO ambition; the Blackstone discussions for high-net-worth clients.

Estimated / third-party

Not figures Revolut has officially disclosed: the stablecoin volume; some World ID operational numbers; the size of the visa-outsourcing market.

Author inference & speculation

Labelled as such in the text: Revolut ID as an external verification rail; the bank-for-banks build; the better Orb; the one redundant room; Storonsky Next.

The factual record the book rests on. Where a primary document is online it is linked; multi-outlet attributions name the outlets without inventing a URL.

- Ian Hogarth, "Can Europe build its first trillion-dollar start-up?" — Financial Times, 30 November 2024 (the book borrows and bends it; it concerns Europe's tech gap broadly, not Revolut). Uncut author's version: ianhogarth.com.

- Revolut's valuation trajectory — the $75bn secondary (Nov 2025), the mooted ~$115bn secondary (June 2026), and the stated IPO ambition of up to $150–200bn (not before 2028). BloombergTechCrunchCoinDesk

- Vlad Yatsenko's move to non-executive director (effective 1 July 2026) and Donato Lucia's move into senior technology leadership. BloombergReutersThe Next Web

- Revolut FY2025 results — ≈$6bn revenue, £1.7bn / $2.3bn pre-tax profit, 68m+ retail and 767k business customers. Revolut Group annual results

- Full UK banking licence (PRA approval, March 2026). PYMNTSBanking Dive

- US national-bank-charter filing (OCC / FDIC, March 2026). FinTech Futures

- MiCA licence and 2025 stablecoin volume. Public reporting

- The PRAGMA foundation model and the Nvidia / Nebius collaboration — Ostroukhov, Mikhailov et al., "PRAGMA: Revolut Foundation Model," arXiv:2604.08649 (9 April 2026); and NVIDIA, "Why Financial Institutions Are Converging on Transaction Foundation Models".

- Private banking — £500,000 threshold, FCA approval (May 2026), and Blackstone partnership discussions. The Next WebBloombergPYMNTScrypto.news

- Ireland penetration and the "I'll Revolut you" usage — Financial Times ("Lessons from Ireland's Revolut revolution"); Irish Times. FTIrish Times

- Digital-document-fraud figures — Entrust, 2025 Identity Fraud Report (digital forgeries crossed 57% of document fraud, +244% YoY).

- Reported discounted share buyback from former staff (December 2025). Finance MagnatesScroll Media

- The ~$185bn figure — card-issuance revenue used as an analogy, not a digital-identity TAM — Ribbit Capital, "Identity" letter (January 2024): ribbitcap.com.

- The ~$22tn of illiquid private assets — Harvard Law School Forum on Corporate Governance, "26 Trends Affecting Capital Markets in 2026" (citing KPMG and Deloitte).

- ESOP-forfeiture figure. PitchBook

- VFS Global — Blackstone's ~75% acquisition for ~$1.87bn (2021), ~$2.5bn valuation. Global Legal ChroniclePTI

- Revolut alumni ventures — Fuse Energy, Sardine, Nevis, Deel — company reporting and the author's own "Revolut Mafia" research: solodkiy.cv/revolut. SiftedTechCrunch

The works behind the academic positioning above — influences and interlocutors, not endorsers.

- Amiti, M., Itskhoki, O., & Konings, J. (2022). Dominant Currencies: How Firms Choose Currency Invoicing and Why It Matters. The Quarterly Journal of Economics, 137(3), 1435–1493. Open-access: NBER Working Paper No. 27926.

- Girotra, K., & Netessine, S. (2014). The Risk-Driven Business Model: Four Questions That Will Define Your Company. Harvard Business Review Press. ISBN 978-1-4221-9153-8.

- Itskhoki, O., & Mukhin, D. (2021). Exchange Rate Disconnect in General Equilibrium. Journal of Political Economy, 129(8), 2183–2232. doi:10.1086/714447.

- King, R. D. (2016). On the Use of Computer Programs as Money. arXiv:1608.00878 · doi:10.48550/arXiv.1608.00878.

- King, R. D., Rowland, J., Oliver, S. G., et al. (2009). The Automation of Science. Science, 324(5923), 85–89. doi:10.1126/science.1165620.

- Tsetlin, I., & Winkler, R. L. (2006). On Equivalent Target-Oriented Formulations for Multiattribute Utility. Decision Analysis, 3(2), 94–99. doi:10.1287/deca.1060.0068.

Further reading — the author's prior work

A book like this doesn't arrive from nowhere. The trail of essays, talks and built prototypes these arguments grew out of — provenance rather than citation.

Essays

- Revolut Is Bigger Than You Think — LinkedIn

- Revolut for Bankrupts, Revolut ID, and 10 More Crazy Ideas — Medium

- What If Revolut Buys WeWork Next Week? — Medium

- The Media Prefers Revolut's Glass Half-Empty — Medium

- Ribbit Capital: Digital Identity Is the New Fintech — LinkedIn

- How Could World ID Be Better? (Or at Least Useful) — LinkedIn

- The Orb's Biometric Panacea Fallacy — Substack

- AI Unicorns and Employee Stock Options — Medium

Talks, decks & podcasts

- Cash Is Still King — ATM Market Research 2023 — SlideShare

- Beyond the Chrome Sphere: Orb Insights of World ID and CLEAR — SlideShare

- A Comprehensive Overview of the Digital Election Market — SlideShare

- Nothing × Teenage Engineering: An AI Mini-Station Concept — SlideShare

- The Orb's Biometric Panacea Fallacy (podcast) — Spotify

- 22 Business Books That Blew My Mind — Tech in Asia

Prototypes & artefacts

- The Revolut Mafia research —

- Digital-identity portfolio —

- World ID Could Be Better — identity.global

- The IOU concept — iou.xxx

- Correspondent banking —

- Compliance and AML —

- The Storonsky Protocol — nikolay.diy

DOI 10.6084/m9.figshare.32782464

ISBN 9798184250809 (hardcover) · 9798184250588 (paperback) · 9798235275867 (ebook)

ASIN B0H6K7FR4K (Kindle)