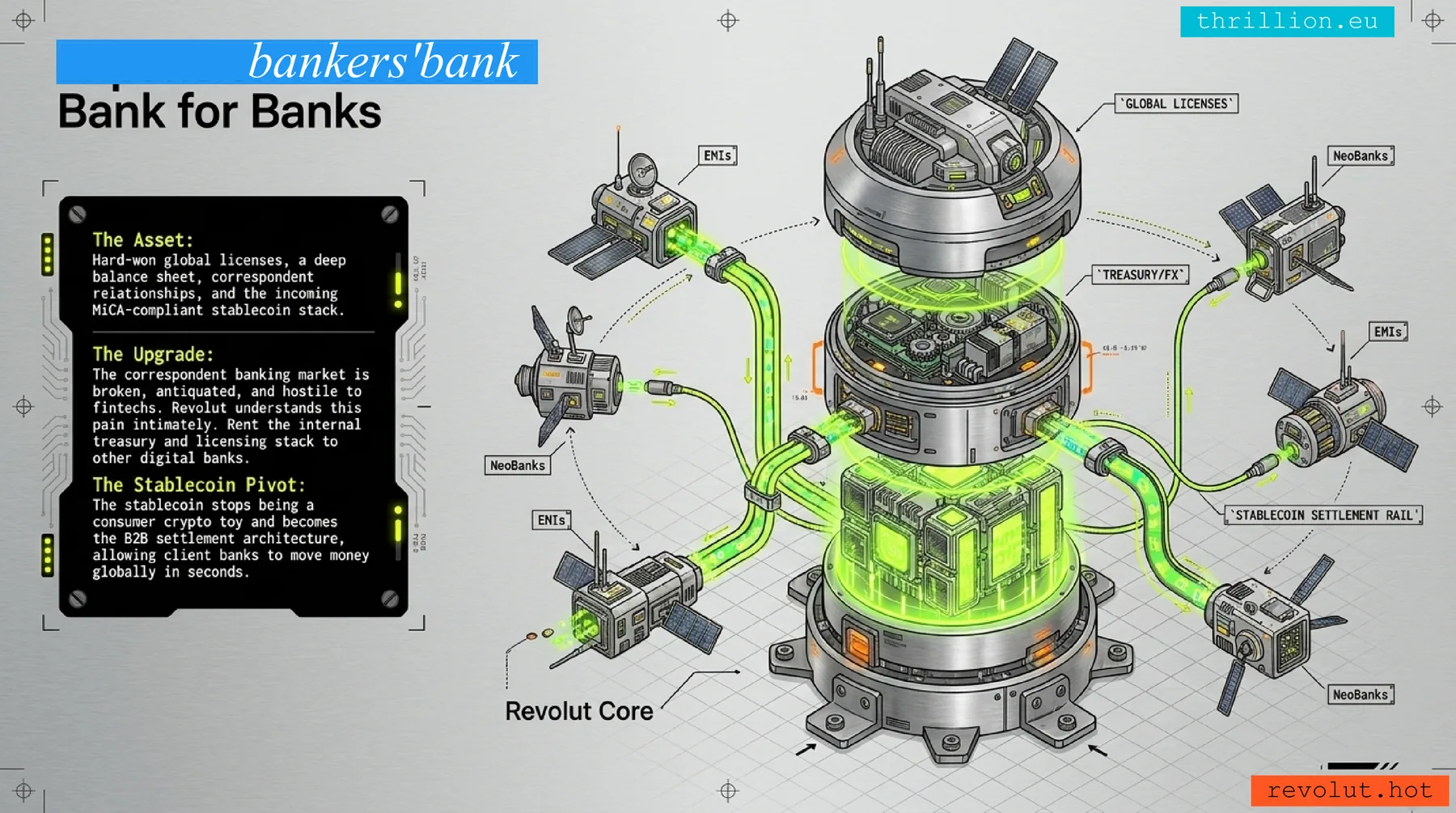

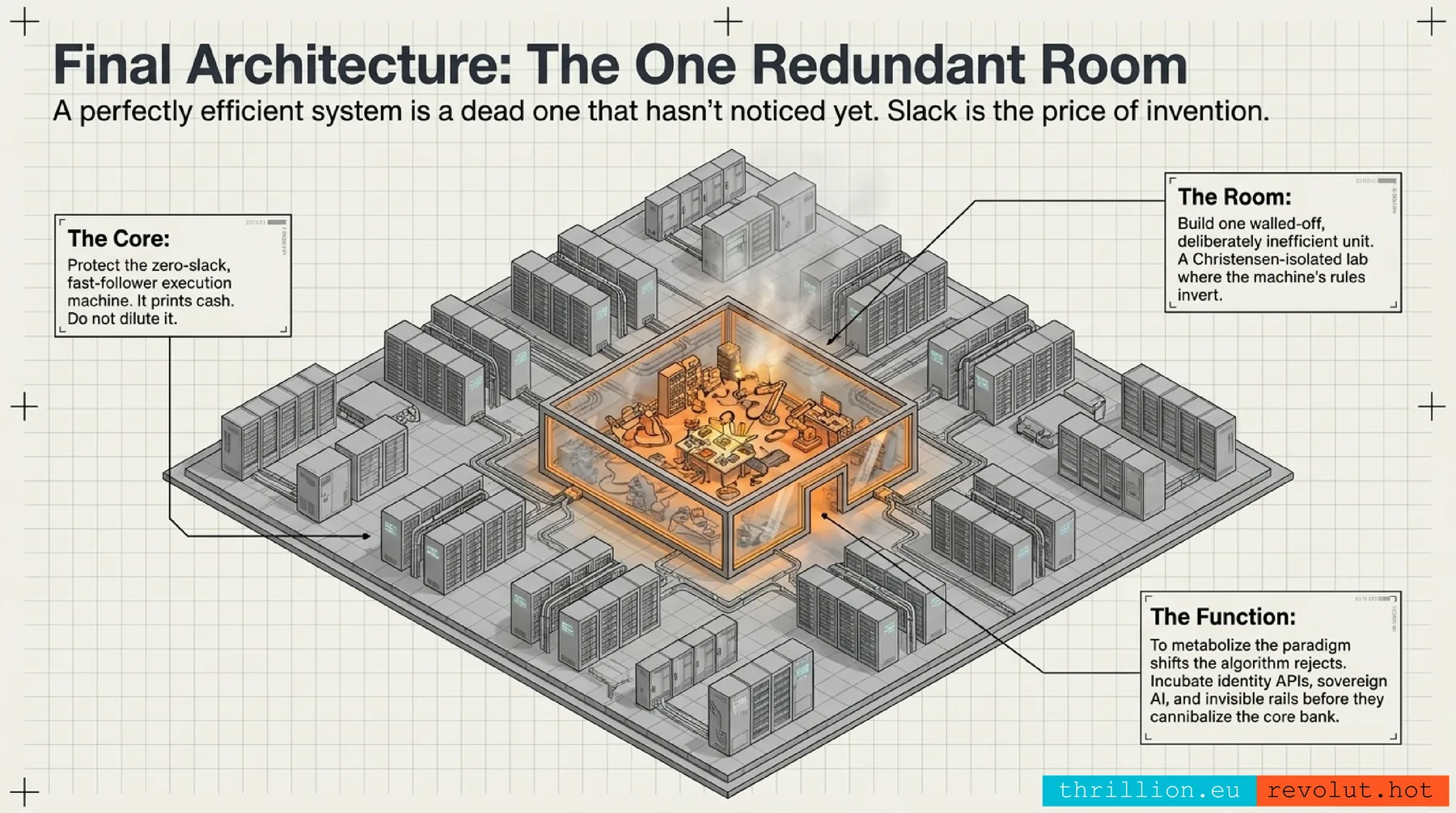

What if? · 01 · The Bank for Banks

The [Digital] Bank for [Digital] Banks

Don't recycle fintech client money into fintech capital. Package regulated infrastructure — safeguarding, agency banking, settlement, treasury and asset-backed credit — for the digital banks, EMIs, IFEs and PSPs that need bank-grade plumbing but don't want to become banks.

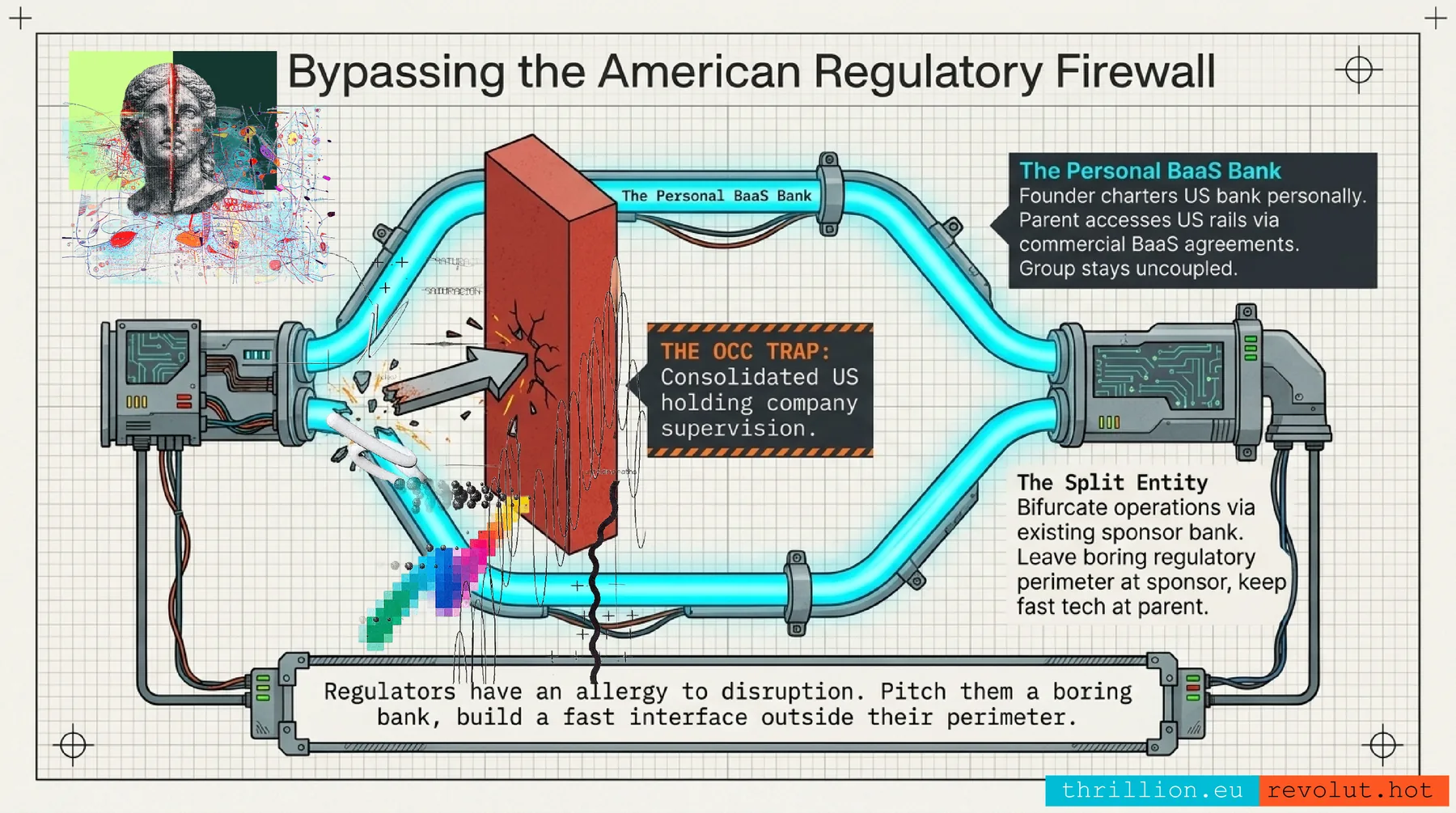

AssetA live UK bank, a pending US national-bank application (OCC, filed Mar 2026) and an EU platform — plus treasury, FX, and a crypto and imminent stablecoin stack.

CopyA BaaS-and-correspondent bank for the fintechs, EMIs and PSPs Revolut used to be one of. Stablecoin-based settlement is already a visible trend, so Revolut enters as a fast-follower with better distribution — not a pioneer taking arrows.

Why nowTougher FCA safeguarding (a CASS-style trust regime is coming); fintechs need settlement, HQLA and balance-sheet partners. The corner is broken and uncontested.

RevenueMake money from trust, movement and risk — in that order: NII on operating balances, flow fees, warehouse credit yield, platform/API pricing.

Product stack — build what supervisors already understand

01

Safeguarding & agency

Named accounts, reconciliations, trust mechanics, reporting for EMIs/PIs.

02

Rails & settlement

Faster Payments, SEPA, cards, ACH/wires, virtual accounts.

03

Treasury & liquidity

Cash concentration, HQLA, intraday funding, FX liquidity.

04

Asset-backed credit

Receivables, card advances, warehouse lines at arm's length.

05

Compliance data

Ledger proof, audit packs, monitoring feeds, source-of-funds.

Evidence hooks Fact

- UK banking licence granted (Mar 2026); US de-novo national-charter filing with the OCC (Mar 2026)

- Revolut already runs US accounts & payments via Lead Bank (Kansas City); FCA finalising CASS-style safeguarding

- MiCA stablecoin rail already live for 1:1 conversion

Risk boundary No-go

- Safeguarded client money is not the EMI's capital — never count it as own funds

- No circular structures that inflate regulatory capital

- Capital and client money stay conceptually separate, always

Correspondent banking only works from the US now. Get the charter right and you don't just win America — you unlock the bankers' bank.